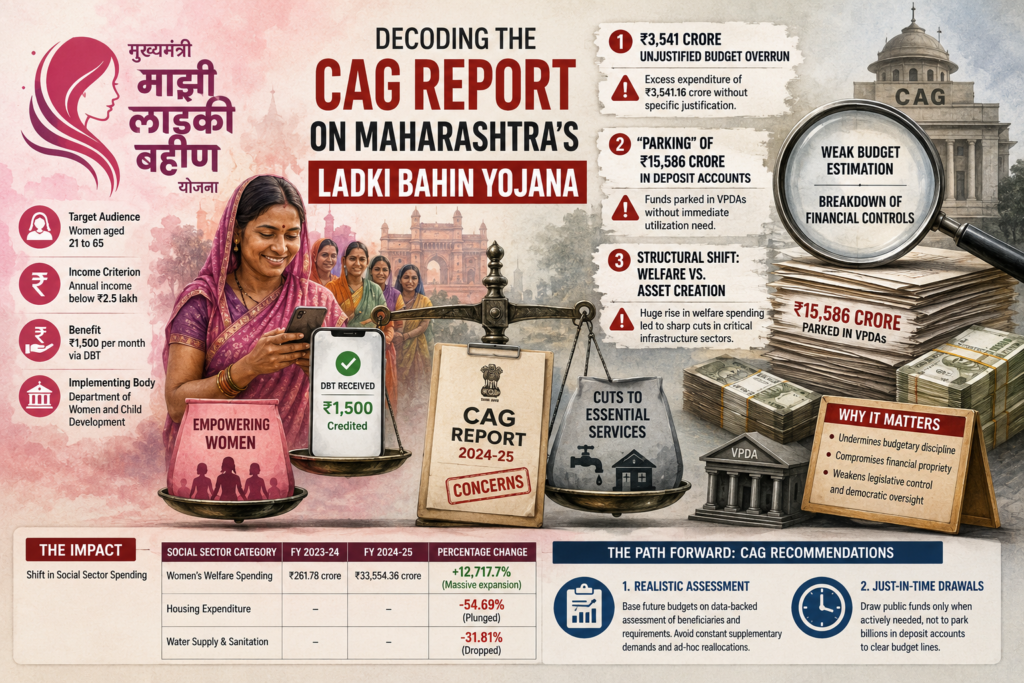

The Comptroller and Auditor General’s (CAG) State Finances Audit Report for the financial year 2024-25 has raised significant concerns regarding the fiscal management of Maharashtra’s flagship Direct Benefit Transfer (DBT) program: the Mukhyamantri Majhi Ladki Bahin Yojana.

While welfare programs are vital social safety nets, the national auditor’s report highlights critical structural risks that emerge when massive cash-transfer schemes are implemented with weak budgetary oversight. This explainer unpacks the key findings, the hidden accounting maneuvers, and the long-term impact on the state’s economic health.

Understanding the Scheme

Launched on June 28, 2024, by the Mahayuti government right ahead of the Assembly elections, the Mukhyamantri Majhi Ladki Bahin Yojana is a targeted cash-transfer scheme.

- Target Audience: Eligible women aged 21 to 65.

- Income Criterion: Families with an annual income below ₹2.5 lakh.

- The Benefit: ₹1,500 per month disbursed directly via Direct Benefit Transfer (DBT).

- Implementing Body: Department of Women and Child Development.

1. The ₹3,541 Crore Unjustified Budget Overrun

The primary red flag raised by the CAG is a massive gap between the officially authorized budget and actual expenditure.

To fund the scheme during 2024-25, the state government pooled resources from multiple avenues:

- ₹26,200 crore allocated through supplementary demands.

- ₹3,490.75 crore re-appropriated from the Lek Ladki Yojana (a scheme providing educational financial assistance to girls from economically weaker backgrounds).

This brought the total authorized grant to ₹29,693.09 crore. However, the Women and Child Development Department ended up spending ₹33,237.24 crore.

The CAG Finding: The department incurred an excess expenditure of ₹3,541.16 crore without providing “any specific justification”. The auditor noted that this reflects weak budget estimation and a breakdown of internal financial controls.

2. The “Parking” of ₹15,586 Crore in Deposit Accounts

Beyond overspending, the audit flagged an accounting maneuver known as the “parking of funds.”

During the final quarter of the financial year (January to March 2025), the department withdrew ₹15,586 crore and transferred it into Virtual Personal Deposit Accounts (VPDA). VPDAs are government-managed accounts used to hold money before it is distributed to final beneficiaries.

The CAG pointed out that there was no immediate utilization requirement for these funds at the time of drawal.

Why does fund parking matter?

When a department draws money from the consolidated fund without immediate spending plans, it artificially inflates expenditure figures for that quarter. The CAG explicitly warned that such practices:

- Undermine the core principles of budgetary discipline.

- Compromise financial propriety.

- Weaken legislative control and democratic oversight over public finances.

3. The Structural Shift: Welfare vs. Asset Creation

Perhaps the most significant long-term takeaway from the CAG report is how this singular massive scheme reshaped Maharashtra’s entire social sector spending portfolio.

Resources are finite. The astronomical rise in spending on women’s welfare directly correlated with a sharp contraction in critical infrastructure and public service investments.

| Social Sector Category | FY 2023-24 Spending | FY 2024-25 Spending | Percentage Change |

|---|---|---|---|

| Women’s Welfare Spending | ₹261.78 crore | ₹33,554.36 crore | +12,717.7% (Massive expansion) |

| Housing Expenditure | — | — | -54.69% (Plunged) |

| Water Supply & Sanitation | — | — | -31.81% (Dropped) |

The CAG observed that this represents a profound policy pivot toward welfare-oriented direct transfers rather than long-term capital formation. While cash transfers offer short-term economic relief to beneficiaries, cutting back on housing, water systems, and sanitation infrastructure risks harming the overall sustainability and quality of essential public service delivery down the line.

The Path Forward: CAG Recommendations

The national auditor’s intent is not to strike down social welfare, but to enforce fiscal accountability. Moving forward, the CAG recommended that the state government implement two crucial corrections:

- Realistic Assessment: Frame future budgets based on a more realistic, data-backed assessment of beneficiary coverage and actual fund requirements. This ensures large DBT schemes do not rely on constant, erratic supplementary demands or ad-hoc fund re-allocations.

- Just-In-Time Drawals: Ensure that public funds are drawn only when they are actively needed for immediate expenditure, rather than letting billions sit idle in deposit accounts to clear out seasonal budget lines.

Watch video: